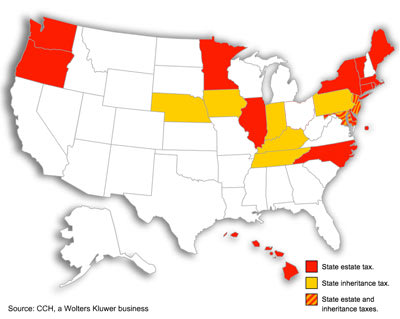

Think you don’t have to worry about estate taxes because of the new generous federal estate tax law? Not so, for families in 21 states and the District of Columbia where separate state levies are still a big concern. “For the vast majority of people who are wealthy, the fear factor of the federal estate tax is gone, but many still need to focus on state estate and inheritance taxes,” says Martin Shenkman, an estate lawyer in Paramus, N.J.

What makes this extra tricky is that state estate and inheritance taxes have been in constant flux over the last decade. And it’s not just the list of states that has been changing, but in some states, the level at which the tax kicks in has been changing (both up and down). So it’s important to stay on top of this to avoid a surprise tax bill.

Thanks to the fiscal cliff tax deal (the American Taxpayer Relief Act), the federal estate tax exemption of a generous $5 million per person, indexed for inflation, is now permanent. So for 2013, up to $5.25 million of an individual’s estate will be exempt from federal estate tax, with a 40% tax rate applied to any excess over the exemption amount.

By contrast, states with estate taxes typically exempt $1 million or less per estate from their tax and impose a top rate of 16%. New York, for example, sets its exemption at $1 million. So the estate of a person dying in New York with $5.25 million would owe no federal tax, but would owe New York $420,800, calculates Donald Hamburg, an estate lawyer with Golenbock Eisenman in New York City.

Six states levy only an inheritance tax, with the rate depending on the relationship of the heir to the deceased and the taxes kicking in, in some cases, on the first dollar of bequest. Two states, Maryland and New Jersey, impose both. Maryland, for example, imposes an estate tax of up to 16% above a $1 million exemption, and a 10% inheritance tax on every dollar left to a niece, nephew, friend or partner, but no inheritance tax on money left to children, grandchildren, parents or siblings. (Any estate tax owed is reduced by the inheritance tax paid.) As in the federal system, bequests to a spouse are tax-free.

Lately, the trend is towards eliminating state estate taxes, or at least lessening the tax bite by increasing the amount exempt from the tax. Ohio no longer has an estate tax, effective Jan. 1, 2013 (Republican Gov. John Kasich signed the repeal law in 2011). Delaware falls off the list effective July 1, 2013 when its current temporary estate tax expires. Indiana’s inheritance tax is repealed effective Jan. 1, 2022 (Republican Gov. Mitch Daniels signed the repeal law last year).

Meanwhile in Indiana the amount that is exempt from the state inheritance tax is going up each year, from $1.25 million this year, to $2 million in 2014 and $5 million in 2015. Other states are upping their exemption amounts this year too. Maine’s exemption doubles to $2 million this year (as part of Republican Gov. Paul LePage’s budget). Rhode Island’s exemption goes up to $910,725 this year, up from $859,350 in 2 012 as it’s indexed for inflation.

Connecticut is the only state going in the other direction recently. In 2011, Connecticut lowered the amount it exempts from its tax from $3.5 million to $2 million per estate, retroactive to Jan. 1, 2011. And Illinois is the most recent state to implement an estate tax—it resurrected an estate tax in 2011 with a $2 million exemption—now $4 million as of Jan. 1, 2013.

The next state to watch out for is North Carolina. Newly elected Rep. Governor Pat McCrory made abolishing the state estate tax one of his campaign promises: “North Carolina is now the only state in the Southeast with the death tax. This tax unfairly punishes those who would inherit their loved one’s possessions or business, forcing some families to sell off a small business or family farm just to pay the tax. As governor, [I] will fight to eliminate the death tax for North Carolinians.”

Could more states add stand-alone estate taxes? A technical provision of the federal estate tax law includes a deduction for state tax paid—instead of the pre-2001 state death tax credit, which allowed states to share in the estate tax revenue the feds collected. For states that were hoping for a return to that revenue sharing, it’s possible that they will consider adding stand-alone taxes, according to James Walschlager, a research analyst at tax publisher CCH, a Wolters Kluwer business.

In the meantime, check out the interactive map showing state estate and inheritance taxes for 2013. Hover over each state to see the dollar amount exempt from taxes and the top rate.

What makes this extra tricky is that state estate and inheritance taxes have been in constant flux over the last decade. And it’s not just the list of states that has been changing, but in some states, the level at which the tax kicks in has been changing (both up and down). So it’s important to stay on top of this to avoid a surprise tax bill.

Thanks to the fiscal cliff tax deal (the American Taxpayer Relief Act), the federal estate tax exemption of a generous $5 million per person, indexed for inflation, is now permanent. So for 2013, up to $5.25 million of an individual’s estate will be exempt from federal estate tax, with a 40% tax rate applied to any excess over the exemption amount.

By contrast, states with estate taxes typically exempt $1 million or less per estate from their tax and impose a top rate of 16%. New York, for example, sets its exemption at $1 million. So the estate of a person dying in New York with $5.25 million would owe no federal tax, but would owe New York $420,800, calculates Donald Hamburg, an estate lawyer with Golenbock Eisenman in New York City.

Six states levy only an inheritance tax, with the rate depending on the relationship of the heir to the deceased and the taxes kicking in, in some cases, on the first dollar of bequest. Two states, Maryland and New Jersey, impose both. Maryland, for example, imposes an estate tax of up to 16% above a $1 million exemption, and a 10% inheritance tax on every dollar left to a niece, nephew, friend or partner, but no inheritance tax on money left to children, grandchildren, parents or siblings. (Any estate tax owed is reduced by the inheritance tax paid.) As in the federal system, bequests to a spouse are tax-free.

Lately, the trend is towards eliminating state estate taxes, or at least lessening the tax bite by increasing the amount exempt from the tax. Ohio no longer has an estate tax, effective Jan. 1, 2013 (Republican Gov. John Kasich signed the repeal law in 2011). Delaware falls off the list effective July 1, 2013 when its current temporary estate tax expires. Indiana’s inheritance tax is repealed effective Jan. 1, 2022 (Republican Gov. Mitch Daniels signed the repeal law last year).

Meanwhile in Indiana the amount that is exempt from the state inheritance tax is going up each year, from $1.25 million this year, to $2 million in 2014 and $5 million in 2015. Other states are upping their exemption amounts this year too. Maine’s exemption doubles to $2 million this year (as part of Republican Gov. Paul LePage’s budget). Rhode Island’s exemption goes up to $910,725 this year, up from $859,350 in 2 012 as it’s indexed for inflation.

Connecticut is the only state going in the other direction recently. In 2011, Connecticut lowered the amount it exempts from its tax from $3.5 million to $2 million per estate, retroactive to Jan. 1, 2011. And Illinois is the most recent state to implement an estate tax—it resurrected an estate tax in 2011 with a $2 million exemption—now $4 million as of Jan. 1, 2013.

The next state to watch out for is North Carolina. Newly elected Rep. Governor Pat McCrory made abolishing the state estate tax one of his campaign promises: “North Carolina is now the only state in the Southeast with the death tax. This tax unfairly punishes those who would inherit their loved one’s possessions or business, forcing some families to sell off a small business or family farm just to pay the tax. As governor, [I] will fight to eliminate the death tax for North Carolinians.”

Could more states add stand-alone estate taxes? A technical provision of the federal estate tax law includes a deduction for state tax paid—instead of the pre-2001 state death tax credit, which allowed states to share in the estate tax revenue the feds collected. For states that were hoping for a return to that revenue sharing, it’s possible that they will consider adding stand-alone taxes, according to James Walschlager, a research analyst at tax publisher CCH, a Wolters Kluwer business.

In the meantime, check out the interactive map showing state estate and inheritance taxes for 2013. Hover over each state to see the dollar amount exempt from taxes and the top rate.

0 comments:

Post a Comment